Many experts currently agree that crypto is no longer subject to such pronounced market cycles, and whether we’re in a bull or bear market is no longer obvious.

Therefore, I think it is not very right to make a decision depending on the current market - this is a matter of speculation, and I propose a general and long-term solution.

The proposed solution is always limited to a $50 million cap, which is reserved to support protocol spending and operational costs

I’m still not convinced. On their own, buybacks don’t really create value - they mostly function as an exit/liquidity event. Without a deeper mechanism linking LDO’s worth to the protocol’s growth, they risk being just a way for holders to cash out.

That’s why I’m especially concerned about crypto droughts - those prolonged stretches of low ETH price. In that environment, the treasury’s value in USD terms shrinks while revenues drop, yet a buyback program would still be pulling funds out (until the lower threshold hits). Even with buffers, a long enough drought could deplete reserves much faster than expected, leaving the DAO underfunded at exactly the time it needs stability most.

Even putting crypto droughts aside, significant swings in ETH’s price could still affect the treasury. They would need to be fairly large swings, but that wouldn’t be unheard of.

Sure, ETH is doing great these days, and all indicators seem to point towards further price increase and adoption of ETH, but we can’t presume that will always be the case.

Maybe I am being overly cautious here, but I think this warrants at least some caution.

Yes, implementing staking is more complex than a buyback. But complexity shouldn’t be a dealbreaker if the end result brings stronger and longer-lasting alignment between the token and the protocol. Designing, auditing, and figuring out governance participation is all solvable - these are normal problems for a DAO of Lido’s size to tackle.

I agree that calculating exact yield can be tricky. But precise yield calculations aren’t the point here. The goal isn’t to promise huge rewards - it’s to give LDO holders a direct, built‑in connection to the protocol’s success.

A dynamic yield model - one that adjusts based on treasury health or ETH performance - could work without guaranteeing massive payouts. Even modest rewards would:

Increase perceived value of LDO

Incentivize buying and holding instead of selling

Promote ongoing governance engagement

Buybacks, by contrast, tend to have the opposite effect: they’re short-lived, externally triggered, and don’t encourage holding or deeper participation.

I’m not convinced that pronounced market cycles are gone - maybe they’re less predictable, but long downturns (“crypto droughts”) have happened before and can easily happen again. The fact that we can’t clearly identify where we are in the cycle actually increases the need to prepare for the worst case.

Granted, I don’t think the “worst case” scenario is even remotely likely, but it would be very arrogant of us to completely dismiss it.

Initial findings from older protocols do not necessarily point to this being true.

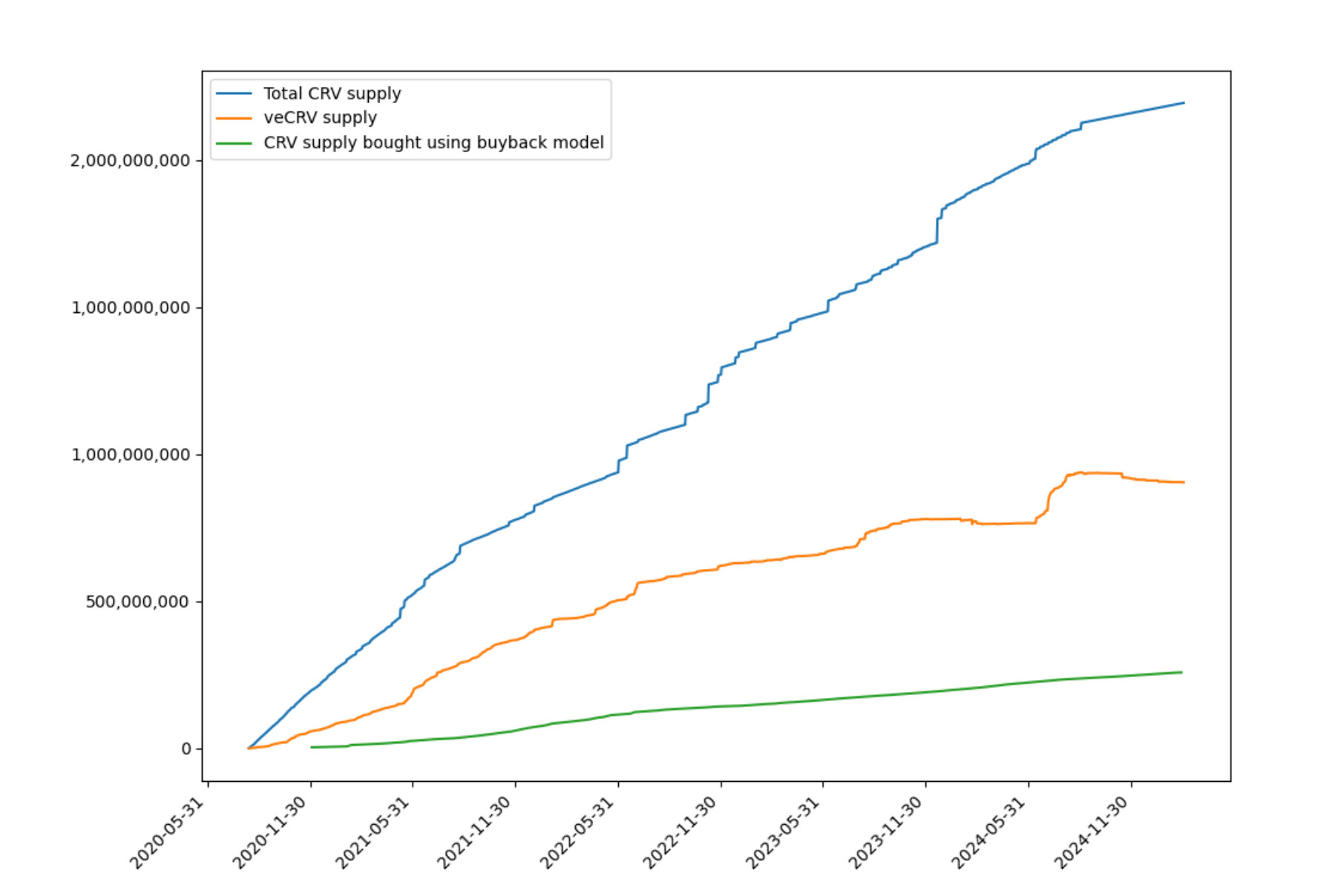

Curve recently published a paper analyzing both buyback-and-burn vs. buyback-and-lock and now after 5 years it’s evident that buyback and lock/stake is having a larger and more positive impact.

A Comparative Analysis of VE-Model and Buyback Model for

“The data reveals that this model locks approximately three times more tokens than would be removed through a burn mechanism (Figure 4), illustrating its superior impact on token scarcity.

Despite the non-permanent nature of veCRV locks, which range from 1 to 4 years with-

out completely removing tokens from circulation, the supply of veCRV has shown steady

growth. This trend indicates that market participants, including aggregators like Convex

Finance, recognize and value the scarcity created by veCRV locking.

Ultimately, while the burn model offers an accessible approach to token scarcity, the

veCRV model, especially when coupled with aggregators, provides a more comprehensive

framework for achieving scarcity and enhancing governance. With three times the token

volume locked in veCRV compared to potential burns, Curve’s veCRV model demon-

strates a robust mechanism for aligning user incentives with protocol growth, indicating

that token locking may hold greater advantages for sustainable DeFi ecosystem develop-

ment.”

Using it as token incentives is far more advantageous (because Lido should still be focused on growth as well as diversifying either horizontally or vertically) only as long as the system is built whereby those who receive those incentives are further incentivised to hold those tokens rather than sell.

You really have well-thought-out questions and concerns.

But this argument is hard for me to understand - I’m proposing to do the buyback only with the surplus above the minimum threshold. If profits fall or go to zero, no buybacks will be carried out

You quoted the part where I talk about how buybacks could affect LDO’s value - but then your answer shifts to surplus buybacks with minimum thresholds. It feels like you are mixing two separate concerns.

One of my concerns is that this effectively sets a low virtual cap for the treasury - assuming continuous buybacks and steady demand for them. ETH’s price will always fluctuate (nothing new there), but under this design, even with a generous buffer zone, the treasury could still end up in the “red zone” after a sharp downturn.

Just because the buyback is from surplus income doesn’t mean the overall treasury is immune to price swings.

Example 1 — Surplus Buybacks

Treasury = $65M, ETH at $3,000. Policy: 50% of new income goes to buybacks.

ETH rises to $30,000 - policy increases to 70% buybacks.

Over this boom period, fees generate $200M - $140M to buybacks, $60M to treasury.

Now the starting $65M treasury is worth $650M (ETH revaluation), plus $60M retained = $710M peak value.

Then a major negative event hits, ETH drops to $1,500 (down 95% from peak).

Treasury after crash: $35.5M, well below a $50M safety threshold.

Example 2 — Fixed % Distribution

Treasury = $65M, ETH at $3,000. Policy: keep 90% of income, distribute 10% to LDO holders.

ETH rises to $30,000 - policy stays the same.

Fees generate $200M - $20M distributed to holders, $180M retained.

Starting $65M treasury is revalued to $650M, plus $180M retained = $830M peak value.

ETH drops to $1,500 - treasury falls to $41.5M.

Still below limit, but ~$4M higher than the surplus buyback case.

Of course, the above examples are only meant to illustrate the issue.

I’m not necessarily advocating for a fixed staking percentage - I only used that in the example for simplicity. In reality, I think a dynamic percentage makes the most sense: higher when ETH and Lido are performing well, and lower when either is under pressure. This approach also allows the treasury to recover more quickly over the long term compared to buybacks.

In both approaches, you’d reach the $50M safety threshold at about the same rate (assuming a 0% staking APY). The key difference is what happens afterwards: fixed-threshold buybacks could slow treasury growth and might lead to intermittent buyback activity - turning on and off as conditions change - whereas a dynamic percentage would keep things smoother and more stable over time.

Maybe I’m missing something, or maybe my assumptions aren’t realistic - but it’s something I noticed and thought was worth pointing out. I’m open to criticism, and it’s entirely possible I’m misunderstanding part of the logic.

I understand your example and for this situation the following solution can be proposed - it is necessary to keep more stables (for example in a ratio of 80/20) in the treasury so that the price of ETH does not greatly affect the balance

Unfortunately, here you can come up with a simple counterexample: if the team spends 95% of the profit, plus 10% on the buyback, then we also get less than the threshold amount, since we end up spending 105%.

Also, this option can lead to the fact that it is quite difficult (as I wrote earlier) to say exactly the profit - this is simply not entirely open information, and therefore there may be disputes and misunderstandings

I think there’s been a slight misunderstanding here - my actual suggestion is not a fixed % distribution model. As I mentioned earlier, I only used the fixed 10% figure in my example to illustrate a different issue, which you addressed in your reply.

I think that the above solution (as far as buybacks are concerned) is a decent one but I would still advocate for something else.

What I’m really proposing is a dynamic % income distribution. This would automatically adjust the retained share of income based on the protocol’s and ETH’s health - keeping more in the treasury during downturns and allowing more distribution in strong markets. This way, we can set clear limits and always ensure the treasury remains above a safety threshold, without the on/off volatility that threshold-based buybacks can create.

A key advantage is that the treasury remains directly linked to ETH price, rather than being influenced by both ETH price and buyback market demand. That’s important because buybacks can behave as a kind of “market timing” tool - they work best when conditions are ideal and can disappear precisely when conditions are worst. Even more importantly, buybacks don’t really incentivize long-term holding or governance involvement. As Marco_112358 notes, they mostly reward those who sell into them, which can actually encourage short-term extraction rather than strengthening the community of engaged token holders.

For these reasons, I just don’t see buybacks as the best way forward for Lido. A dynamic % distribution model is simpler, more predictable, and better aligned with maintaining treasury health and incentivising holders who actively participate in governance.