Welcome to March’s reWARDS budget.

Details are below as usual. This proposal will be open for community feedback for 3 days. After which, if there is no contention, it will be acted upon.

As always, if there are budget updates throughout the month, they will be posted under this topic for transparency.

The sections are as follows:

- Important Updates

- Budget and breakdown

- Network Specific Comments

Important Updates:

-

The most notable update and difference in March’s budget is that there are zero budgeted incentives for both stDOT and stKSM (on Moonbeam and Moonriver respectively). Rewards on these two chains were not distributed in February already, and are now not present in this budget. The rows pertaining to these networks are still included here (at zero) for readability and accounting reasons – and will not appear on reWARDS’ budgets from April’s onwards.

-

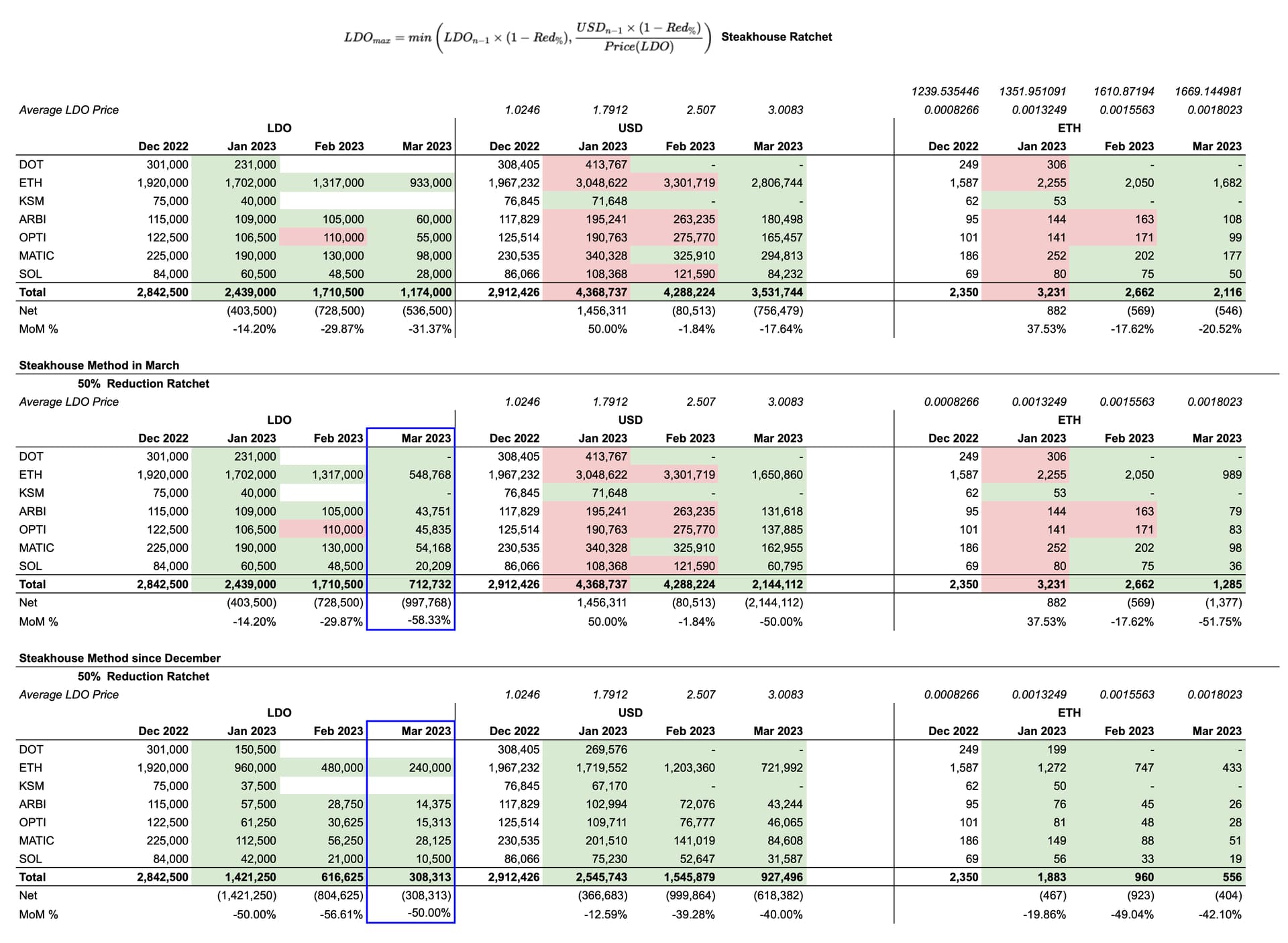

This budget lists all rewards line items in both LDO and USD, thanks to @stakehouse’s suggestion. This allows for both points of view to be easily accessible by Lido’s community and DAO members.

-

New incentives have been included for incentivizing wstETH’s boostrapping of liquidity and utility on Polygon. These are under Polygon’s budget.

-

In this budget, @stakehouse’s proposal of ratcheting down the amount of rewards in both LDO and USD (instead of just in LDO independently of market price) was heard. There are strategic, growth and market considerations that may make it infeasible to rigidly stick to it, but it will be directionally implemented.

- February’s reWARDS budget requested 1,890,000 LDO at a (then) market price of $4,347,000 while March’s requests 1,096,000 LDO at a 30d-twap market price of $2,747,672

Budget and Breakdown

March’23’s budget calls for 1,291,400 LDO. (Actual 1,174,000 + 10% buffer)

Remaining balances estimated at EOM (unspent and left in the different multisigs by the last day of February and usable for March’s incentives, rounded to thousands):

- Ethereum: 119,000 LDO

- Solana: 49,000 LDO

- Polygon: 0 LDO

- Moonbeam (Polkadot): 0 LDO

- Moonriver (Kusama): 0 LDO

- Arbitrum: 16,000 LDO

- Optimism: 12,000 LDO

- Total: 196,000 LDO

Requested budget 1,096,000 (Budget Call - Remaining, rounded)

(At a LDO 30d-twap, this amount has a market price of ~$2,747,672)

- To be distributed across the following pools and networks with the buffer of 117,400 LDO held for unaccounted needs during the month.

- The detailed .csv file is provided here.

Network Specific Comments:

Ethereum

The considerations from last month stand for this one with the special consideration that LDO/ETH price has increased which justifies not needing as many LDO budgeted for the same amount of ETH liquidity.

As such, the gradual reduction in incentives has continued in this budget.

Solana

No specific comments.

Polkadot & Kusama

As mentioned above, February was the first month in which liquidity and integrations for both stDOT on Moonbeam and stKSM on Moonriver were not incentivized. The committee has been tracking the effects of these cuts in order to extrapolate learnings to other networks/parts of the budgets.

Polygon

wstETH expansion on Polygon increasing DeFi diversity on chain, deepening liquidity and improving composability.

Arbitrum & Optimism

In February we saw continued adoption of wstETH on Arbitrum and Optimism. Highlights included the launch of new Beefy vaults, a new Dopex Vault, new Premia vaults, the launch of the wstETH market on Granary, and more.

Users of wstETH on Layer 2 networks will see some very exciting developments in March. Currently it is anticipated that Aave will list wstETH on Aave V3 on both Optimism and Arbitrum. It is also anticipated that Radiant, GMX, JonesDAO, QiDAO, TraderJoe, Vesta, Lyra, Perpetual, and more will have new wstETH integrations and/or markets for wstETH users.

Other notes:

LDO incentives on dFORCE are currently paused following the exploit of the wstETH-ETH LP market. This exploit having been resolved we anticipate the unpausing of rewards for the wstETH market only. dFORCE will use the remaining LDO allocated to them from the February budget so no new allocation has been made for March

As always, any feedback, questions and comments are welcomed!