Hi, I’m Ouroboros Capital, most commonly known for my Twitter profile. I am a holder of LDO tokens and have briefly tweeted about how I think Lido can benefit from an investment in CVX but would like to elaborate here. I would like to propose for Lido to consider a plan to purchase CVX such that it can solve for the currently unsustainable emissions of LDO tokens into stETH liquidity pools. Disclaimer: I am also a holder of CVX.

Why not AURA?

Before we start, I’d like to preface by saying that given AURA’s still inflationary nature which, as a result, leads to the unpredictability of vlAURA’s future APR, I’ll be focusing on CVX. Additionally, AURA’s lack of liquidity – trades $350K/day on Balancer, means its less pragmatic at this point for it to be considered as a solution for size of LDO’s emission woes. This compares to vs CVX which i) trades $3.5mn/day on Binance, ii) trades $2.8mn/day on Curve and iii) and has existing holders such as Terra (~$10mn CVX holder) which may look to get out via an OTC trade.

The Current Situation – stETH deep liquidity is important but Lido’s current incentives can only last 4 years.

Lido’s key value proposition is the readily available on-chain liquidity on stETH that it provides. However, LDO currently spends ~4.5mn LDO (~$6.3mn) in emissions monthly/54mn LDO ($75.6mn) in emissions annually to sustain these liquidity pools. While it is paramount that LDO maintains its core value proposition of having deep on-chain liquidity venues for stETH, it needs to work towards a sustainable solution for its stETH on-chain liquidity. LDO treasury only has ~$260mn (mostly LDO with some stETH, DAI and ETH) which means at the current run rate, it would last less than 4 years before running out of incentives.

ReWARDS Team is looking this, but we need to accelerate the process as its an opportune time to accumulate CVX.

While the rewards committee has acknowledged “the need to optimize the current program” and has put out a detailed post on its consideration when it comes to incentives optimization, I’m hoping that this post would provide information that would augment as well as accelerate that process given that CVX is currently trading below its intrinsic value – in other words, an opportune window presents itself for Lido to accumulate CVX.

Own CVX as a sustainable solution to the emission issue

The rewards team has already covered in Update on Rewards, a good introduction on how owning CVX would be an investment that would pay off over time (through wielding $CVX/$CRV emissions as as compared to the DAO spending its precious $LDO tokens). The reWARDS committee has also elaborated that the “next steps here would be to discount that back (accounting for opportunity cost) + account for price risk of being effectively long that position as a DAO”. I’m hoping to provide points that would aid that analysis.

2 Key Considerations when owning CVX vs bribing/paying own emissions.

-

Payback Period – How long for the investment in $CVX to pay off in terms of directable emissions.

-

$CVX/$CRV price relative to $LDO price and the outlook for that – if $CVX/CRV price is expected to rise vs $LDO then the investment in $CVX vs paying $LDO as reward incentives would be much more effective.

How long does it take for $CVX to payback?

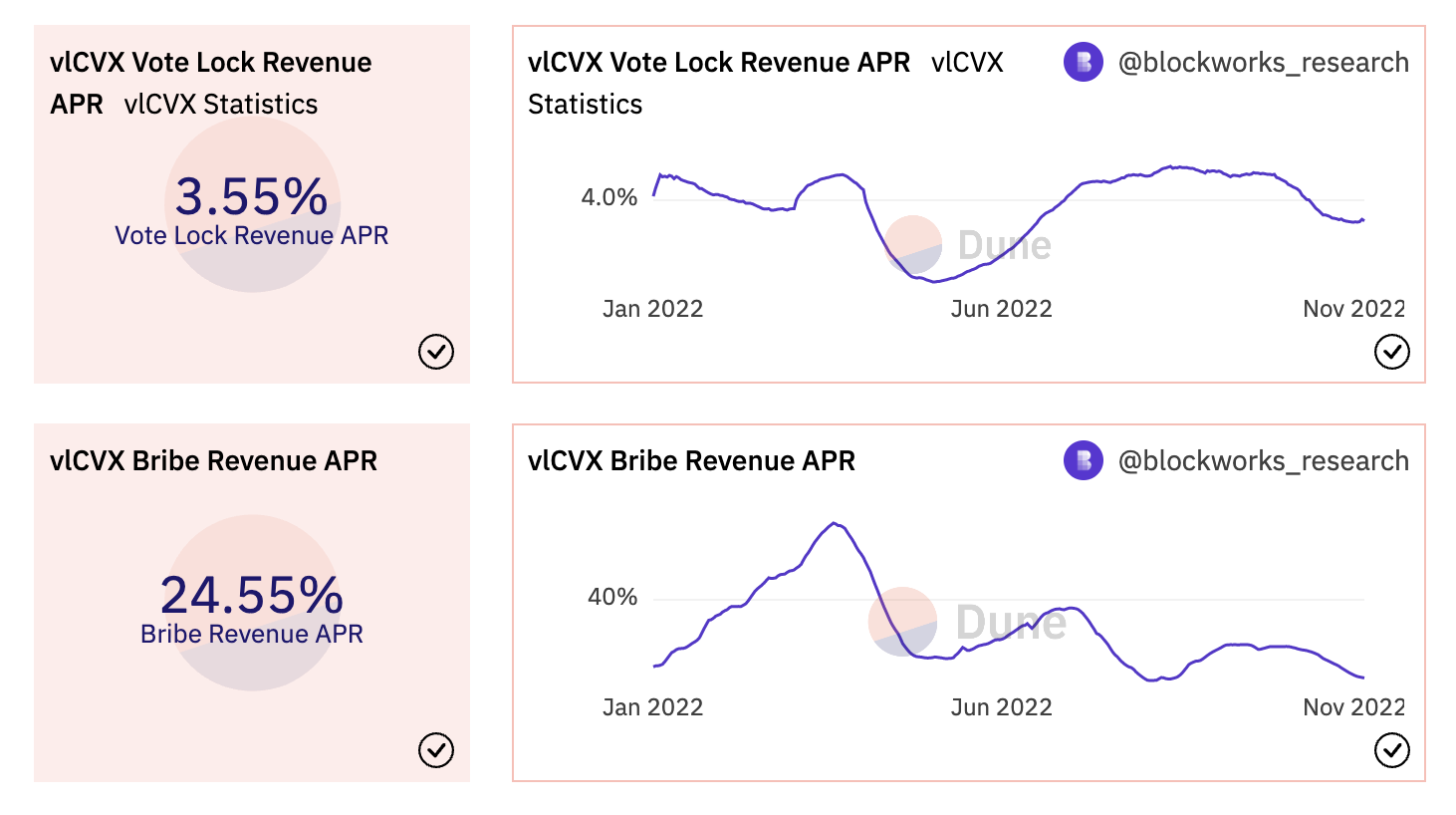

According to Llama Airforce, $ value of emission that $1 of CVX wields (based on the latest round of bribes) is as follows:

$1 of CVX wields 39c of CRV+CVX emissions (annualized) – vlCVX APR of 31% * $1.25 emission per $1 of bribe. In other words, a payback period of ~2.5 years (closer to 3.5 years post adjusting for the declining CVX emissions in the next few years).

How does the outlook of $CRV/$CVX price looks compared to $LDO.

Price = intersection of supply (inflation + sellers) and demand (buyers). The outlook of a token’s price is often an exercise involving pontification. However, I will attempt here to be as methodical as possible, comparing the supply and demand dynamics of the two tokens relative to each other.

On the supply side, I will compare both token’s inflation outlook relative to their liquidity profiles.

On the demand side, both token’s potential demand sources as well as imminent developments (narrative). And finally netting the two against both token’s liquidity.

TOKEN PRICE OUTLOOK - SUPPLY SIDE ANALYSIS

Inflation of CVX – CVX is close to the end of its emission to depositors on Convex. One year forward, there will only be ~9mn CVX ($44mn) emitted to LPs on CVX (mostly to LP token depositors on Convex as well as cvxCRV). Contrasting that to on-chain liquidity venues – selling $1mn of CVX on-chain would incur a 5.9% slippage. Furthermore, it is worth noting that the Frax-3CRV and Frax-BP both in totality ~20% of Curve weekly gauge weights and ~66% of the above-mentioned Frax pools are Frax protocol owned liquidity. Frax has committed in its governance to fully accumulate all CVX going into its protocol owned Frax pool, thereby absorbing a small % of these emissions.

Inflation of LDO – One year forward, based on the existing reWARDS budget, Lido would have spent ~54mn LDO ($75.6mn). Contrasting that to existing off-chain liquidity venues – selling $1mn of LDO on-chain would incur a 5.5% slippage.

Contrasting LDO and CVX’s inflation and comparing it to the current liquidity, Lido has inflation close to 2x the multitude of CVX with similar liquidity profiles and as such on the supply side more likely to experience price pressure. This is not yet considering the above-mentioned “Frax effect”.

TOKEN PRICE OUTLOOK - DEMAND SIDE ANALYSIS

-

CVX’s underlying asset CRV is on the cusp of releasing crvUSD which based on teasers so far suggest a new CDP revenue vertical and likely to lift the underlying value accrual of CRV and consequently CVX.

-

LDO as of now is largely a governance token with little value accrual (ie. no real yield) vs CVX which serves as an outsourced emission management mechanism for protocols is likely to see greater demand pockets.

-

Post the Merge narrative, there is a lack of impetus for speculators to buy LDO.

**In conclusion, combining both supply and demand analysis, CVX and CRV appears to have a higher likelihood of outperforming Lido, thereby positioning it as a favorable investment for the DAO vs spending Lido tokens as reward incentives. Worth noting too that the ratio of CVX and CRV token price vs LDO is at the low end of the range.

Flywheel from Investing in CVX and Reduced LDO Emissions

While there is unlikely sufficient liquidity in CVX and AURA for Lido to fully replace LDO emissions, the partial replacement of LDO emissions would still stem downward pressure in token price to some extent and as such boost $ value of each LDO token. As such, over and above creating a sustainable solution to incentivizing stETH liquidity pools via, the number of LDO emitted per month would also be indirectly reduced from an uplift in the token price.

CRV/CVX wars is protocol (3,3)

I’ve tweet about this before as well. The CRV/CVX wars are essentially (3,3) for protocols. More diamond handed protocols (eg. Frax) joining CVX/CRV cartel will essentially absorb circulating supply and lift price of CVX/CRV. In other words, being an early mover would see greater dividends being paid on the investment. Another point for consideration.

CONCLUSION

I am a holder of LDO as I see it as a great business - sitting on a lion share of the staked ETH market as well as being a core DeFi lego/infrastructure. That said, token price is being heavily pressured by rewards into stETH pools which I hope LDO can solve through my suggestion. I believe my suggestions have presented a good case as to why CVX/CRV are good investments presently relative to LDO price and Lido spending LDO tokens as incentives. I’ve presented many points here that I’m more than happy to discuss with the reWARDS team or even be part of the team to help push this through. Feel free to hit me up on Twitter.